Volmaster FX historical tools

This feature presents high quality analytics on the historical behavior of ccy pairs, both for realized (sampled) volatility and implied (quoted) volatility.

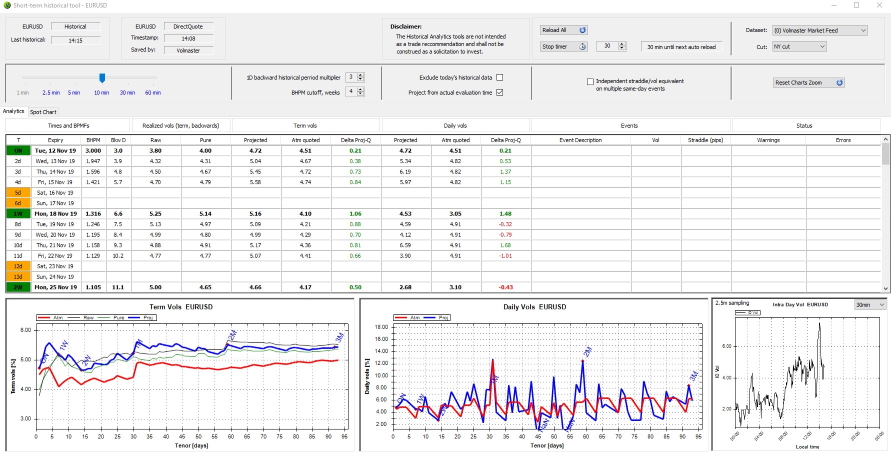

The short-term tool allows traders to have measures of the intraday granular volatility realization and therefore provide an estimation for quoting short-dated options and optimizing gamma-related trades. The tool includes adjustments for realized economic events of the past as well as the management of expected economic events of the near future.

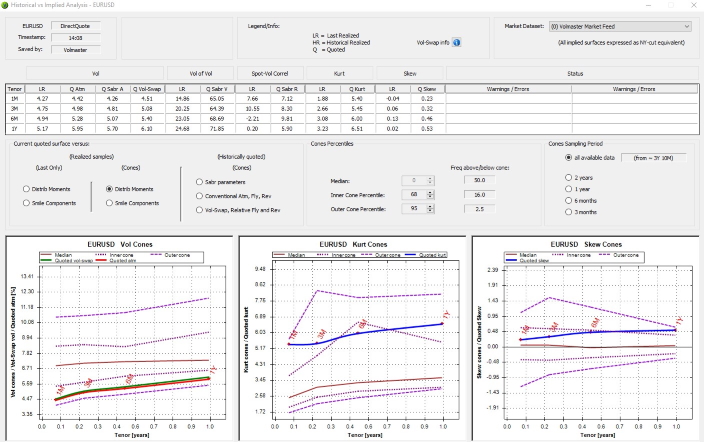

The long-term volatility tool allows traders to view and chart several measures, such as the realized moments of the sampled spot prices (volatility, skew, kurtosis) as well as interpret such measures in terms of stochastic volatility parameters (vol-of-vol, spot-vol correlation). Information can then be represented in terms of cones and compared with the current measures implied from the quoted volatility surface.

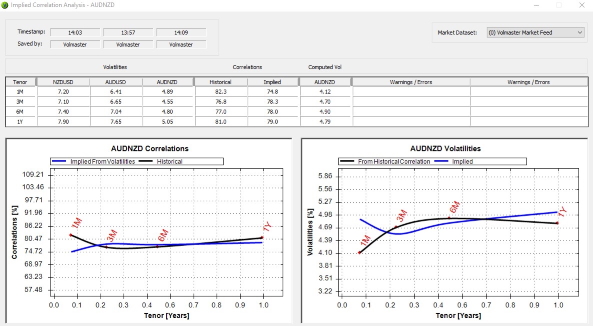

The correlation tool allows traders to get a measure of the historical correlation among all ccypairs. The tool can also be used in conjunction with our correlation wizard in order to quote illiquid pairs via copulas.

Our tools provide unvaluable insights in the historical behavior of ccypairs and as such a tremendous added value for all traders.

Request more information

Please contact us for further information about Volmaster FX technology: info@volmaster.com